Michael E. Porter is the Bishop William Lawrence University Professor at Harvard University, based at Harvard Business School in Boston. He is a six-time McKinsey Award winner, including for his most recent HBR article, “Strategy and Society,” coauthored with Mark R. Kramer (December 2006).

If the forces are intense, as they are in such industries as airlines, textiles, and hotels, almost no company earns attractive returns on investment. If the forces are benign, as they are in industries such as software, soft drinks, and toiletries, many companies are profitable. Industry structure drives competition and profitability, not whether an industry produces a product or service, is emerging or mature, high tech or low tech, regulated or unregulated. While a myriad of factors can affect industry profitability in the short run—including the weather and the business cycle—industry structure, manifested in the competitive forces, sets industry profitability in the medium and long run. (See the exhibit “Differences in Industry Profitability.”)

Differences in Industry Profitability

Understanding the competitive forces, and their underlying causes, reveals the roots of an industry’s current profitability while providing a framework for anticipating and influencing competition (and profitability) over time. A healthy industry structure should be as much a competitive concern to strategists as their company’s own position. Understanding industry structure is also essential to effective strategic positioning. As we will see, defending against the competitive forces and shaping them in a company’s favor are crucial to strategy.

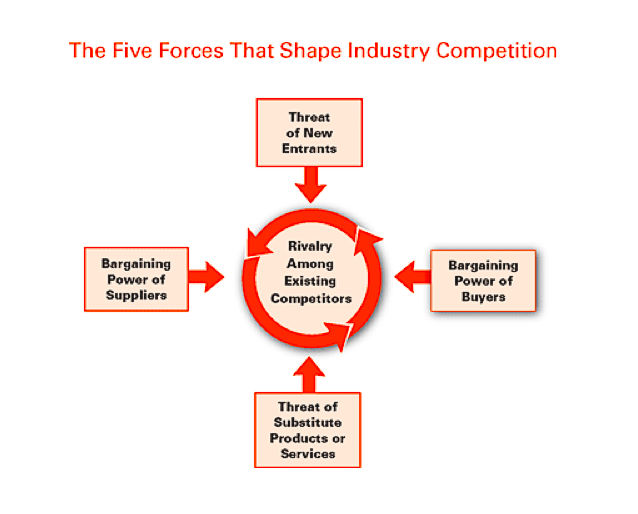

Forces That Shape Competition

The configuration of the five forces differs by industry. In the market for commercial aircraft, fierce rivalry between dominant producers Airbus and Boeing and the bargaining power of the airlines that place huge orders for aircraft are strong, while the threat of entry, the threat of substitutes, and the power of suppliers are more benign. In the movie theater industry, the proliferation of substitute forms of entertainment and the power of the movie producers and distributors who supply movies, the critical input, are important.

The strongest competitive force or forces determine the profitability of an industry and become the most important to strategy formulation. The most salient force, however, is not always obvious.

For example, even though rivalry is often fierce in commodity industries, it may not be the factor limiting profitability. Low returns in the photographic film industry, for instance, are the result of a superior substitute product—as Kodak and Fuji, the world’s leading producers of photographic film, learned with the advent of digital photography. In such a situation, coping with the substitute product becomes the number one strategic priority.

Industry structure grows out of a set of economic and technical characteristics that determine the strength of each competitive force. We will examine these drivers in the pages that follow, taking the perspective of an incumbent, or a company already present in the industry. The analysis can be readily extended to understand the challenges facing a potential entrant.

New entrants to an industry bring new capacity and a desire to gain market share that puts pressure on prices, costs, and the rate of investment necessary to compete. Particularly when new entrants are diversifying from other markets, they can leverage existing capabilities and cash flows to shake up competition, as Pepsi did when it entered the bottled water industry, Microsoft did when it began to offer internet browsers, and Apple did when it entered the music distribution business.

The threat of entry, therefore, puts a cap on the profit potential of an industry. When the threat is high, incumbents must hold down their prices or boost investment to deter new competitors. In specialty coffee retailing, for example, relatively low entry barriers mean that Starbucks must invest aggressively in modernizing stores and menus.

The threat of entry in an industry depends on the height of entry barriers that are present and on the reaction entrants can expect from incumbents. If entry barriers are low and newcomers expect little retaliation from the entrenched competitors, the threat of entry is high and industry profitability is moderated. It is the threat of entry, not whether entry actually occurs, that holds down profitability.

Barriers to entry.

Entry barriers are advantages that incumbents have relative to new entrants. There are seven major sources:

1. Supply-side economies of scale. These economies arise when firms that produce at larger volumes enjoy lower costs per unit because they can spread fixed costs over more units, employ more efficient technology, or command better terms from suppliers. Supply-side scale economies deter entry by forcing the aspiring entrant either to come into the industry on a large scale, which requires dislodging entrenched competitors, or to accept a cost disadvantage.

Scale economies can be found in virtually every activity in the value chain; which ones are most important varies by industry.1 In microprocessors, incumbents such as Intel are protected by scale economies in research, chip fabrication, and consumer marketing. For lawn care companies like Scotts Miracle-Gro, the most important scale economies are found in the supply chain and media advertising. In small-package delivery, economies of scale arise in national logistical systems and information technology.

2. Demand-side benefits of scale. These benefits, also known as network effects, arise in industries where a buyer’s willingness to pay for a company’s product increases with the number of other buyers who also patronize the company. Buyers may trust larger companies more for a crucial product: Recall the old adage that no one ever got fired for buying from IBM (when it was the dominant computer maker). Buyers may also value being in a “network” with a larger number of fellow customers. For instance, online auction participants are attracted to eBay because it offers the most potential trading partners. Demand-side benefits of scale discourage entry by limiting the willingness of customers to buy from a newcomer and by reducing the price the newcomer can command until it builds up a large base of customers.

3. Customer switching costs. Switching costs are fixed costs that buyers face when they change suppliers. Such costs may arise because a buyer who switches vendors must, for example, alter product specifications, retrain employees to use a new product, or modify processes or information systems. The larger the switching costs, the harder it will be for an entrant to gain customers. Enterprise resource planning (ERP) software is an example of a product with very high switching costs. Once a company has installed SAP’s ERP system, for example, the costs of moving to a new vendor are astronomical because of embedded data, the fact that internal processes have been adapted to SAP, major retraining needs, and the mission-critical nature of the applications.

4. Capital requirements. The need to invest large financial resources in order to compete can deter new entrants. Capital may be necessary not only for fixed facilities but also to extend customer credit, build inventories, and fund start-up losses. The barrier is particularly great if the capital is required for unrecoverable and therefore harder-to-finance expenditures, such as up-front advertising or research and development. While major corporations have the financial resources to invade almost any industry, the huge capital requirements in certain fields limit the pool of likely entrants. Conversely, in such fields as tax preparation services or short-haul trucking, capital requirements are minimal and potential entrants plentiful.

It is important not to overstate the degree to which capital requirements alone deter entry. If industry returns are attractive and are expected to remain so, and if capital markets are efficient, investors will provide entrants with the funds they need. For aspiring air carriers, for instance, financing is available to purchase expensive aircraft because of their high resale value, one reason why there have been numerous new airlines in almost every region.

5. Incumbency advantages independent of size. No matter what their size, incumbents may have cost or quality advantages not available to potential rivals. These advantages can stem from such sources as proprietary technology, preferential access to the best raw material sources, preemption of the most favorable geographic locations, established brand identities, or cumulative experience that has allowed incumbents to learn how to produce more efficiently. Entrants try to bypass such advantages. Upstart discounters such as Target and Wal-Mart, for example, have located stores in freestanding sites rather than regional shopping centers where established department stores were well entrenched.

6. Unequal access to distribution channels. The new entrant must, of course, secure distribution of its product or service. A new food item, for example, must displace others from the supermarket shelf via price breaks, promotions, intense selling efforts, or some other means. The more limited the wholesale or retail channels are and the more that existing competitors have tied them up, the tougher entry into an industry will be. Sometimes access to distribution is so high a barrier that new entrants must bypass distribution channels altogether or create their own. Thus, upstart low-cost airlines have avoided distribution through travel agents (who tend to favor established higher-fare carriers) and have encouraged passengers to book their own flights on the internet.

7. Restrictive government policy. Government policy can hinder or aid new entry directly, as well as amplify (or nullify) the other entry barriers. Government directly limits or even forecloses entry into industries through, for instance, licensing requirements and restrictions on foreign investment. Regulated industries like liquor retailing, taxi services, and airlines are visible examples.

Government policy can heighten other entry barriers through such means as expansive patenting rules that protect proprietary technology from imitation or environmental or safety regulations that raise scale economies facing newcomers. Of course, government policies may also make entry easier—directly through subsidies, for instance, or indirectly by funding basic research and making it available to all firms, new and old, reducing scale economies.

Entry barriers should be assessed relative to the capabilities of potential entrants, which may be start-ups, foreign firms, or companies in related industries. And, as some of our examples illustrate, the strategist must be mindful of the creative ways newcomers might find to circumvent apparent barriers.

Expected retaliation.

How potential entrants believe incumbents may react will also influence their decision to enter or stay out of an industry. If reaction is vigorous and protracted enough, the profit potential of participating in the industry can fall below the cost of capital. Incumbents often use public statements and responses to one entrant to send a message to other prospective entrants about their commitment to defending market share.

Newcomers are likely to fear expected retaliation if:

Incumbents have previously responded vigorously to new entrants.

Incumbents possess substantial resources to fight back, including excess cash and unused borrowing power, available productive capacity, or clout with distribution channels and customers.

Incumbents seem likely to cut prices because they are committed to retaining market share at all costs or because the industry has high fixed costs, which create a strong motivation to drop prices to fill excess capacity.

Industry growth is slow so newcomers can gain volume only by taking it from incumbents.

An analysis of barriers to entry and expected retaliation is obviously crucial for any company contemplating entry into a new industry. The challenge is to find ways to surmount the entry barriers without nullifying, through heavy investment, the profitability of participating in the industry.

The power of suppliers.

Powerful suppliers capture more of the value for themselves by charging higher prices, limiting quality or services, or shifting costs to industry participants. Powerful suppliers, including suppliers of labor, can squeeze profitability out of an industry that is unable to pass on cost increases in its own prices. Microsoft, for instance, has contributed to the erosion of profitability among personal computer makers by raising prices on operating systems. PC makers, competing fiercely for customers who can easily switch among them, have limited freedom to raise their prices accordingly.

Companies depend on a wide range of different supplier groups for inputs. A supplier group is powerful if:

It is more concentrated than the industry it sells to. Microsoft’s near monopoly in operating systems, coupled with the fragmentation of PC assemblers, exemplifies this situation.

The supplier group does not depend heavily on the industry for its revenues. Suppliers serving many industries will not hesitate to extract maximum profits from each one. If a particular industry accounts for a large portion of a supplier group’s volume or profit, however, suppliers will want to protect the industry through reasonable pricing and assist in activities such as R&D and lobbying.

Industry participants face switching costs in changing suppliers. For example, shifting suppliers is difficult if companies have invested heavily in specialized ancillary equipment or in learning how to operate a supplier’s equipment (as with Bloomberg terminals used by financial professionals). Or firms may have located their production lines adjacent to a supplier’s manufacturing facilities (as in the case of some beverage companies and container manufacturers). When switching costs are high, industry participants find it hard to play suppliers off against one another. (Note that suppliers may have switching costs as well. This limits their power.)

Suppliers offer products that are differentiated. Pharmaceutical companies that offer patented drugs with distinctive medical benefits have more power over hospitals, health maintenance organizations, and other drug buyers, for example, than drug companies offering me-too or generic products.

There is no substitute for what the supplier group provides. Pilots’ unions, for example, exercise considerable supplier power over airlines partly because there is no good alternative to a well-trained pilot in the cockpit.

The supplier group can credibly threaten to integrate forward into the industry. In that case, if industry participants make too much money relative to suppliers, they will induce suppliers to enter the market.

The power of buyers.

Powerful customers—the flip side of powerful suppliers—can capture more value by forcing down prices, demanding better quality or more service (thereby driving up costs), and generally playing industry participants off against one another, all at the expense of industry profitability. Buyers are powerful if they have negotiating leverage relative to industry participants, especially if they are price sensitive, using their clout primarily to pressure price reductions.

As with suppliers, there may be distinct groups of customers who differ in bargaining power. A customer group has negotiating leverage if:

There are few buyers, or each one purchases in volumes that are large relative to the size of a single vendor. Large-volume buyers are particularly powerful in industries with high fixed costs, such as telecommunications equipment, offshore drilling, and bulk chemicals. High fixed costs and low marginal costs amplify the pressure on rivals to keep capacity filled through discounting.

The industry’s products are standardized or undifferentiated. If buyers believe they can always find an equivalent product, they tend to play one vendor against another.

Buyers face few switching costs in changing vendors.

Buyers can credibly threaten to integrate backward and produce the industry’s product themselves if vendors are too profitable. Producers of soft drinks and beer have long controlled the power of packaging manufacturers by threatening to make, and at times actually making, packaging materials themselves.

A buyer group is price sensitive if:

The product it purchases from the industry represents a significant fraction of its cost structure or procurement budget. Here buyers are likely to shop around and bargain hard, as consumers do for home mortgages. Where the product sold by an industry is a small fraction of buyers’ costs or expenditures, buyers are usually less price sensitive.

The buyer group earns low profits, is strapped for cash, or is otherwise under pressure to trim its purchasing costs. Highly profitable or cash-rich customers, in contrast, are generally less price sensitive (that is, of course, if the item does not represent a large fraction of their costs).

The quality of buyers’ products or services is little affected by the industry’s product. Where quality is very much affected by the industry’s product, buyers are generally less price sensitive. When purchasing or renting production quality cameras, for instance, makers of major motion pictures opt for highly reliable equipment with the latest features. They pay limited attention to price.

The industry’s product has little effect on the buyer’s other costs. Here, buyers focus on price. Conversely, where an industry’s product or service can pay for itself many times over by improving performance or reducing labor, material, or other costs, buyers are usually more interested in quality than in price. Examples include products and services like tax accounting or well logging (which measures below-ground conditions of oil wells) that can save or even make the buyer money. Similarly, buyers tend not to be price sensitive in services such as investment banking, where poor performance can be costly and embarrassing.

Most sources of buyer power apply equally to consumers and to business-to-business customers. Like industrial customers, consumers tend to be more price sensitive if they are purchasing products that are undifferentiated, expensive relative to their incomes, and of a sort where product performance has limited consequences. The major difference with consumers is that their needs can be more intangible and harder to quantify.

Intermediate customers, or customers who purchase the product but are not the end user (such as assemblers or distribution channels), can be analyzed the same way as other buyers, with one important addition. Intermediate customers gain significant bargaining power when they can influence the purchasing decisions of customers downstream. Consumer electronics retailers, jewelry retailers, and agricultural-equipment distributors are examples of distribution channels that exert a strong influence on end customers.

Producers often attempt to diminish channel clout through exclusive arrangements with particular distributors or retailers or by marketing directly to end users. Component manufacturers seek to develop power over assemblers by creating preferences for their components with downstream customers. Such is the case with bicycle parts and with sweeteners. DuPont has created enormous clout by advertising its Stainmaster brand of carpet fibers not only to the carpet manufacturers that actually buy them but also to downstream consumers. Many consumers request Stainmaster carpet even though DuPont is not a carpet manufacturer.

The threat of substitutes.

A substitute performs the same or a similar function as an industry’s product by a different means. Videoconferencing is a substitute for travel. Plastic is a substitute for aluminum. E-mail is a substitute for express mail. Sometimes, the threat of substitution is downstream or indirect, when a substitute replaces a buyer industry’s product. For example, lawn-care products and services are threatened when multifamily homes in urban areas substitute for single-family homes in the suburbs. Software sold to agents is threatened when airline and travel websites substitute for travel agents.

Substitutes are always present, but they are easy to overlook because they may appear to be very different from the industry’s product: To someone searching for a Father’s Day gift, neckties and power tools may be substitutes. It is a substitute to do without, to purchase a used product rather than a new one, or to do it yourself (bring the service or product in-house).

When the threat of substitutes is high, industry profitability suffers. Substitute products or services limit an industry’s profit potential by placing a ceiling on prices. If an industry does not distance itself from substitutes through product performance, marketing, or other means, it will suffer in terms of profitability—and often growth potential.

Substitutes not only limit profits in normal times, they also reduce the bonanza an industry can reap in good times. In emerging economies, for example, the surge in demand for wired telephone lines has been capped as many consumers opt to make a mobile telephone their first and only phone line.

The threat of a substitute is high if:

It offers an attractive price-performance trade-off to the industry’s product. The better the relative value of the substitute, the tighter is the lid on an industry’s profit potential. For example, conventional providers of long-distance telephone service have suffered from the advent of inexpensive internet-based phone services such as Vonage and Skype. Similarly, video rental outlets are struggling with the emergence of cable and satellite video-on-demand services, online video rental services such as Netflix, and the rise of internet video sites like Google’s YouTube.

The buyer’s cost of switching to the substitute is low. Switching from a proprietary, branded drug to a generic drug usually involves minimal costs, for example, which is why the shift to generics (and the fall in prices) is so substantial and rapid.

Strategists should be particularly alert to changes in other industries that may make them attractive substitutes when they were not before. Improvements in plastic materials, for example, allowed them to substitute for steel in many automobile components. In this way, technological changes or competitive discontinuities in seemingly unrelated businesses can have major impacts on industry profitability. Of course the substitution threat can also shift in favor of an industry, which bodes well for its future profitability and growth potential.

Rivalry among existing competitors.

Rivalry among existing competitors takes many familiar forms, including price discounting, new product introductions, advertising campaigns, and service improvements. High rivalry limits the profitability of an industry. The degree to which rivalry drives down an industry’s profit potential depends, first, on the intensity with which companies compete and, second, on the basis on which they compete.

The intensity of rivalry is greatest if:

Competitors are numerous or are roughly equal in size and power. In such situations, rivals find it hard to avoid poaching business. Without an industry leader, practices desirable for the industry as a whole go unenforced.

Industry growth is slow. Slow growth precipitates fights for market share.

Exit barriers are high. Exit barriers, the flip side of entry barriers, arise because of such things as highly specialized assets or management’s devotion to a particular business. These barriers keep companies in the market even though they may be earning low or negative returns. Excess capacity remains in use, and the profitability of healthy competitors suffers as the sick ones hang on.

Rivals are highly committed to the business and have aspirations for leadership, especially if they have goals that go beyond economic performance in the particular industry. High commitment to a business arises for a variety of reasons. For example, state-owned competitors may have goals that include employment or prestige. Units of larger companies may participate in an industry for image reasons or to offer a full line. Clashes of personality and ego have sometimes exaggerated rivalry to the detriment of profitability in fields such as the media and high technology. Firms cannot read each other’s signals well because of lack of familiarity with one another, diverse approaches to competing, or differing goals. The strength of rivalry reflects not just the intensity of competition but also the basis of competition. The dimensions on which competition takes place, and whether rivals converge to compete on the same dimensions, have a major influence on profitability.

Rivalry is especially destructive to profitability if it gravitates solely to price because price competition transfers profits directly from an industry to its customers. Price cuts are usually easy for competitors to see and match, making successive rounds of retaliation likely. Sustained price competition also trains customers to pay less attention to product features and service.

Price competition is most liable to occur if:

Products or services of rivals are nearly identical and there are few switching costs for buyers. This encourages competitors to cut prices to win new customers. Years of airline price wars reflect these circumstances in that industry.

Fixed costs are high and marginal costs are low. This creates intense pressure for competitors to cut prices below their average costs, even close to their marginal costs, to steal incremental customers while still making some contribution to covering fixed costs. Many basic-materials businesses, such as paper and aluminum, suffer from this problem, especially if demand is not growing. So do delivery companies with fixed networks of routes that must be served regardless of volume.

Capacity must be expanded in large increments to be efficient. The need for large capacity expansions, as in the polyvinyl chloride business, disrupts the industry’s supply-demand balance and often leads to long and recurring periods of overcapacity and price cutting.

The product is perishable. Perishability creates a strong temptation to cut prices and sell a product while it still has value. More products and services are perishable than is commonly thought. Just as tomatoes are perishable because they rot, models of computers are perishable because they soon become obsolete, and information may be perishable if it diffuses rapidly or becomes outdated, thereby losing its value. Services such as hotel accommodations are perishable in the sense that unused capacity can never be recovered.

Competition on dimensions other than price—on product features, support services, delivery time, or brand image, for instance—is less likely to erode profitability because it improves customer value and can support higher prices. Also, rivalry focused on such dimensions can improve value relative to substitutes or raise the barriers facing new entrants. While non price rivalry sometimes escalates to levels that undermine industry profitability, this is less likely to occur than it is with price rivalry.

As important as the dimensions of rivalry is whether rivals compete on the same dimensions. When all or many competitors aim to meet the same needs or compete on the same attributes, the result is zero-sum competition. Here, one firm’s gain is often another’s loss, driving down profitability. While price competition runs a stronger risk than non price competition of becoming zero sum, this may not happen if companies take care to segment their markets, targeting their low-price offerings to different customers.

Rivalry can be positive sum, or actually increase the average profitability of an industry, when each competitor aims to serve the needs of different customer segments, with different mixes of price, products, services, features, or brand identities. Such competition can not only support higher average profitability but also expand the industry, as the needs of more customer groups are better met. The opportunity for positive-sum competition will be greater in industries serving diverse customer groups. With a clear understanding of the structural underpinnings of rivalry, strategists can sometimes take steps to shift the nature of competition in a more positive direction.

Factors, Not Forces

Industry structure, as manifested in the strength of the five competitive forces, determines the industry’s long-run profit potential because it determines how the economic value created by the industry is divided—how much is retained by companies in the industry versus bargained away by customers and suppliers, limited by substitutes, or constrained by potential new entrants. By considering all five forces, a strategist keeps overall structure in mind instead of gravitating to any one element. In addition, the strategist’s attention remains focused on structural conditions rather than on fleeting factors.

It is especially important to avoid the common pitfall of mistaking certain visible attributes of an industry for its underlying structure. Consider the following:

Industry growth rate.

A common mistake is to assume that fast-growing industries are always attractive. Growth does tend to mute rivalry, because an expanding pie offers opportunities for all competitors. But fast growth can put suppliers in a powerful position, and high growth with low entry barriers will draw in entrants. Even without new entrants, a high growth rate will not guarantee profitability if customers are powerful or substitutes are attractive. Indeed, some fast-growth businesses, such as personal computers, have been among the least profitable industries in recent years. A narrow focus on growth is one of the major causes of bad strategy decisions.

Technology and innovation.

Advanced technology or innovations are not by themselves enough to make an industry structurally attractive (or unattractive). Mundane, low-technology industries with price-insensitive buyers, high switching costs, or high entry barriers arising from scale economies are often far more profitable than sexy industries, such as software and internet technologies, that attract competitors.

Government is not best understood as a sixth force because government involvement is neither inherently good nor bad for industry profitability. The best way to understand the influence of government on competition is to analyze how specific government policies affect the five competitive forces. For instance, patents raise barriers to entry, boosting industry profit potential. Conversely, government policies favoring unions may raise supplier power and diminish profit potential. Bankruptcy rules that allow failing companies to reorganize rather than exit can lead to excess capacity and intense rivalry. Government operates at multiple levels and through many different policies, each of which will affect structure in different ways.

Complementary products and services.

Complements are products or services used together with an industry’s product. Complements arise when the customer benefit of two products combined is greater than the sum of each product’s value in isolation. Computer hardware and software, for instance, are valuable together and worthless when separated.

In recent years, strategy researchers have highlighted the role of complements, especially in high-technology industries where they are most obvious.3 By no means, however, do complements appear only there. The value of a car, for example, is greater when the driver also has access to gasoline stations, roadside assistance, and auto insurance.

Complements can be important when they affect the overall demand for an industry’s product. However, like government policy, complements are not a sixth force determining industry profitability since the presence of strong complements is not necessarily bad (or good) for industry profitability. Complements affect profitability through the way they influence the five forces.

The strategist must trace the positive or negative influence of complements on all five forces to ascertain their impact on profitability. The presence of complements can raise or lower barriers to entry. In application software, for example, barriers to entry were lowered when producers of complementary operating system software, notably Microsoft, provided tool sets making it easier to write applications. Conversely, the need to attract producers of complements can raise barriers to entry, as it does in video game hardware.

The presence of complements can also affect the threat of substitutes. For instance, the need for appropriate fueling stations makes it difficult for cars using alternative fuels to substitute for conventional vehicles. But complements can also make substitution easier. For example, Apple’s iTunes hastened the substitution from CDs to digital music.

Complements can factor into industry rivalry either positively (as when they raise switching costs) or negatively (as when they neutralize product differentiation). Similar analyses can be done for buyer and supplier power. Sometimes companies compete by altering conditions in complementary industries in their favor, such as when videocassette-recorder producer JVC persuaded movie studios to favor its standard in issuing prerecorded tapes even though rival Sony’s standard was probably superior from a technical standpoint.

Identifying complements is part of the analyst’s work. As with government policies or important technologies, the strategic significance of complements will be best understood through the lens of the five forces.

Changes in Industry Structure

So far, we have discussed the competitive forces at a single point in time. Industry structure proves to be relatively stable, and industry profitability differences are remarkably persistent over time in practice. However, industry structure is constantly undergoing modest adjustment—and occasionally it can change abruptly.

Shifts in structure may emanate from outside an industry or from within. They can boost the industry’s profit potential or reduce it. They may be caused by changes in technology, changes in customer needs, or other events. The five competitive forces provide a framework for identifying the most important industry developments and for anticipating their impact on industry attractiveness.

Shifting threat of new entry.

Changes to any of the seven barriers described above can raise or lower the threat of new entry. The expiration of a patent, for instance, may unleash new entrants. On the day that Merck’s patents for the cholesterol reducer Zocor expired, three pharmaceutical makers entered the market for the drug. Conversely, the proliferation of products in the ice cream industry has gradually filled up the limited freezer space in grocery stores, making it harder for new ice cream makers to gain access to distribution in North America and Europe.

Strategic decisions of leading competitors often have a major impact on the threat of entry. Starting in the 1970s, for example, retailers such as Wal-Mart, Kmart, and Toys “R” Us began to adopt new procurement, distribution, and inventory control technologies with large fixed costs, including automated distribution centers, bar coding, and point-of-sale terminals. These investments increased the economies of scale and made it more difficult for small retailers to enter the business (and for existing small players to survive).

Changing supplier or buyer power.

As the factors underlying the power of suppliers and buyers change with time, their clout rises or declines. In the global appliance industry, for instance, competitors including Electrolux, General Electric, and Whirlpool have been squeezed by the consolidation of retail channels (the decline of appliance specialty stores, for instance, and the rise of big-box retailers like Best Buy and Home Depot in the United States). Another example is travel agents, who depend on airlines as a key supplier. When the internet allowed airlines to sell tickets directly to customers, this significantly increased their power to bargain down agents’ commissions.

Shifting threat of substitution.

The most common reason substitutes become more or less threatening over time is that advances in technology create new substitutes or shift price-performance comparisons in one direction or the other. The earliest microwave ovens, for example, were large and priced above $2,000, making them poor substitutes for conventional ovens. With technological advances, they became serious substitutes. Flash computer memory has improved enough recently to become a meaningful substitute for low-capacity hard-disk drives. Trends in the availability or performance of complementary producers also shift the threat of substitutes.

New bases of rivalry.

Rivalry often intensifies naturally over time. As an industry matures, growth slows. Competitors become more alike as industry conventions emerge, technology diffuses, and consumer tastes converge. Industry profitability falls, and weaker competitors are driven from the business. This story has played out in industry after industry; televisions, snowmobiles, and telecommunications equipment are just a few examples.

A trend toward intensifying price competition and other forms of rivalry, however, is by no means inevitable. For example, there has been enormous competitive activity in the U.S. casino industry in recent decades, but most of it has been positive-sum competition directed toward new niches and geographic segments (such as riverboats, trophy properties, Native American reservations, international expansion, and novel customer groups like families). Head-to-head rivalry that lowers prices or boosts the payouts to winners has been limited.

The nature of rivalry in an industry is altered by mergers and acquisitions that introduce new capabilities and ways of competing. Or, technological innovation can reshape rivalry. In the retail brokerage industry, the advent of the internet lowered marginal costs and reduced differentiation, triggering far more intense competition on commissions and fees than in the past.

In some industries, companies turn to mergers and consolidation not to improve cost and quality but to attempt to stop intense competition. Eliminating rivals is a risky strategy, however. The five competitive forces tell us that a profit windfall from removing today’s competitors often attracts new competitors and backlash from customers and suppliers. In New York banking, for example, the 1980s and 1990s saw escalating consolidations of commercial and savings banks, including Manufacturers Hanover, Chemical, Chase, and Dime Savings. But today the retail-banking landscape of Manhattan is as diverse as ever, as new entrants such as Wachovia, Bank of America, and Washington Mutual have entered the market.

Implications for Strategy

Understanding the forces that shape industry competition is the starting point for developing strategy. Every company should already know what the average profitability of its industry is and how that has been changing over time. The five forces reveal why industry profitability is what it is. Only then can a company incorporate industry conditions into strategy.

The forces reveal the most significant aspects of the competitive environment. They also provide a baseline for sizing up a company’s strengths and weaknesses: Where does the company stand versus buyers, suppliers, entrants, rivals, and substitutes? Most importantly, an understanding of industry structure guides managers toward fruitful possibilities for strategic action, which may include any or all of the following: positioning the company to better cope with the current competitive forces; anticipating and exploiting shifts in the forces; and shaping the balance of forces to create a new industry structure that is more favorable to the company. The best strategies exploit more than one of these possibilities.

Positioning the company.

Strategy can be viewed as building defenses against the competitive forces or finding a position in the industry where the forces are weakest. Consider, for instance, the position of Paccar in the market for heavy trucks. The heavy-truck industry is structurally challenging. Many buyers operate large fleets or are large leasing companies, with both the leverage and the motivation to drive down the price of one of their largest purchases. Most trucks are built to regulated standards and offer similar features, so price competition is rampant. Capital intensity causes rivalry to be fierce, especially during the recurring cyclical downturns. Unions exercise considerable supplier power. Though there are few direct substitutes for an 18-wheeler, truck buyers face important substitutes for their services, such as cargo delivery by rail.

In this setting, Paccar, a Bellevue, Washington–based company with about 20% of the North American heavy-truck market, has chosen to focus on one group of customers: owner-operators—drivers who own their trucks and contract directly with shippers or serve as subcontractors to larger trucking companies. Such small operators have limited clout as truck buyers. They are also less price sensitive because of their strong emotional ties to and economic dependence on the product. They take great pride in their trucks, in which they spend most of their time.

Paccar has invested heavily to develop an array of features with owner-operators in mind: luxurious sleeper cabins, plush leather seats, noise-insulated cabins, sleek exterior styling, and so on. At the company’s extensive network of dealers, prospective buyers use software to select among thousands of options to put their personal signature on their trucks. These customized trucks are built to order, not to stock, and delivered in six to eight weeks. Paccar’s trucks also have aerodynamic designs that reduce fuel consumption, and they maintain their resale value better than other trucks. Paccar’s roadside assistance program and IT-supported system for distributing spare parts reduce the time a truck is out of service. All these are crucial considerations for an owner-operator. Customers pay Paccar a 10% premium, and its Kenworth and Peterbilt brands are considered status symbols at truck stops.

Paccar illustrates the principles of positioning a company within a given industry structure. The firm has found a portion of its industry where the competitive forces are weaker—where it can avoid buyer power and price-based rivalry. And it has tailored every single part of the value chain to cope well with the forces in its segment. As a result, Paccar has been profitable for 68 years straight and has earned a long-run return on equity above 20%.

In addition to revealing positioning opportunities within an existing industry, the five forces framework allows companies to rigorously analyze entry and exit. Both depend on answering the difficult question: “What is the potential of this business?” Exit is indicated when industry structure is poor or declining and the company has no prospect of a superior positioning. In considering entry into a new industry, creative strategists can use the framework to spot an industry with a good future before this good future is reflected in the prices of acquisition candidates. Five forces analysis may also reveal industries that are not necessarily attractive for the average entrant but in which a company has good reason to believe it can surmount entry barriers at lower cost than most firms or has a unique ability to cope with the industry’s competitive forces.

Exploiting industry change.

Industry changes bring the opportunity to spot and claim promising new strategic positions if the strategist has a sophisticated understanding of the competitive forces and their underpinnings. Consider, for instance, the evolution of the music industry during the past decade. With the advent of the internet and the digital distribution of music, some analysts predicted the birth of thousands of music labels (that is, record companies that develop artists and bring their music to market). This, the analysts argued, would break a pattern that had held since Edison invented the phonograph: Between three and six major record companies had always dominated the industry. The internet would, they predicted, remove distribution as a barrier to entry, unleashing a flood of new players into the music industry.

A careful analysis, however, would have revealed that physical distribution was not the crucial barrier to entry. Rather, entry was barred by other benefits that large music labels enjoyed. Large labels could pool the risks of developing new artists over many bets, cushioning the impact of inevitable failures. Even more important, they had advantages in breaking through the clutter and getting their new artists heard. To do so, they could promise radio stations and record stores access to well-known artists in exchange for promotion of new artists. New labels would find this nearly impossible to match. The major labels stayed the course, and new music labels have been rare.

This is not to say that the music industry is structurally unchanged by digital distribution. Unauthorized downloading created an illegal but potent substitute. The labels tried for years to develop technical platforms for digital distribution themselves, but major companies hesitated to sell their music through a platform owned by a rival. Into this vacuum stepped Apple with its iTunes music store, launched in 2003 to support its iPod music player. By permitting the creation of a powerful new gatekeeper, the major labels allowed industry structure to shift against them. The number of major record companies has actually declined—from six in 1997 to four today—as companies struggled to cope with the digital phenomenon.

When industry structure is in flux, new and promising competitive positions may appear. Structural changes open up new needs and new ways to serve existing needs. Established leaders may overlook these or be constrained by past strategies from pursuing them. Smaller competitors in the industry can capitalize on such changes, or the void may well be filled by new entrants.

Shaping industry structure.

When a company exploits structural change, it is recognizing, and reacting to, the inevitable. However, companies also have the ability to shape industry structure. A firm can lead its industry toward new ways of competing that alter the five forces for the better. In reshaping structure, a company wants its competitors to follow so that the entire industry will be transformed. While many industry participants may benefit in the process, the innovator can benefit most if it can shift competition in directions where it can excel.

An industry’s structure can be reshaped in two ways: by redividing profitability in favor of incumbents or by expanding the overall profit pool. Redividing the industry pie aims to increase the share of profits to industry competitors instead of to suppliers, buyers, substitutes, and keeping out potential entrants. Expanding the profit pool involves increasing the overall pool of economic value generated by the industry in which rivals, buyers, and suppliers can all share.

Redividing profitability.

To capture more profits for industry rivals, the starting point is to determine which force or forces are currently constraining industry profitability and address them. A company can potentially influence all of the competitive forces. The strategist’s goal here is to reduce the share of profits that leak to suppliers, buyers, and substitutes or are sacrificed to deter entrants.

To neutralize supplier power, for example, a firm can standardize specifications for parts to make it easier to switch among suppliers. It can cultivate additional vendors, or alter technology to avoid a powerful supplier group altogether. To counter customer power, companies may expand services that raise buyers’ switching costs or find alternative means of reaching customers to neutralize powerful channels. To temper profit-eroding price rivalry, companies can invest more heavily in unique products, as pharmaceutical firms have done, or expand support services to customers. To scare off entrants, incumbents can elevate the fixed cost of competing—for instance, by escalating their R&D or marketing expenditures. To limit the threat of substitutes, companies can offer better value through new features or wider product accessibility. When soft-drink producers introduced vending machines and convenience store channels, for example, they dramatically improved the availability of soft drinks relative to other beverages.

Sysco, the largest food-service distributor in North America, offers a revealing example of how an industry leader can change the structure of an industry for the better. Food-service distributors purchase food and related items from farmers and food processors. They then warehouse and deliver these items to restaurants, hospitals, employer cafeterias, schools, and other food-service institutions.

Given low barriers to entry, the food-service distribution industry has historically been highly fragmented, with numerous local competitors. While rivals try to cultivate customer relationships, buyers are price sensitive because food represents a large share of their costs. Buyers can also choose the substitute approaches of purchasing directly from manufacturers or using retail sources, avoiding distributors altogether. Suppliers wield bargaining power: They are often large companies with strong brand names that food preparers and consumers recognize. Average profitability in the industry has been modest.

Sysco recognized that, given its size and national reach, it might change this state of affairs. It led the move to introduce private-label distributor brands with specifications tailored to the food-service market, moderating supplier power. Sysco emphasized value-added services to buyers such as credit, menu planning, and inventory management to shift the basis of competition away from just price. These moves, together with stepped-up investments in information technology and regional distribution centers, substantially raised the bar for new entrants while making the substitutes less attractive. Not surprisingly, the industry has been consolidating, and industry profitability appears to be rising.

Industry leaders have a special responsibility for improving industry structure. Doing so often requires resources that only large players possess. Moreover, an improved industry structure is a public good because it benefits every firm in the industry, not just the company that initiated the improvement. Often, it is more in the interests of an industry leader than any other participant to invest for the common good because leaders will usually benefit the most. Indeed, improving the industry may be a leader’s most profitable strategic opportunity, in part because attempts to gain further market share can trigger strong reactions from rivals, customers, and even suppliers.

There is a dark side to shaping industry structure that is equally important to understand. Ill-advised changes in competitive positioning and operating practices can undermine industry structure. Faced with pressures to gain market share or enamored with innovation for its own sake, managers may trigger new kinds of competition that no incumbent can win. When taking actions to improve their own company’s competitive advantage, then, strategists should ask whether they are setting in motion dynamics that will undermine industry structure in the long run. In the early days of the personal computer industry, for instance, IBM tried to make up for its late entry by offering an open architecture that would set industry standards and attract complementary makers of application software and peripherals. In the process, it ceded ownership of the critical components of the PC—the operating system and the microprocessor—to Microsoft and Intel. By standardizing PCs, it encouraged price-based rivalry and shifted power to suppliers. Consequently, IBM became the temporarily dominant firm in an industry with an enduringly unattractive structure.

Expanding the profit pool.

When overall demand grows, the industry’s quality level rises, intrinsic costs are reduced, or waste is eliminated, the pie expands. The total pool of value available to competitors, suppliers, and buyers grows. The total profit pool expands, for example, when channels become more competitive or when an industry discovers latent buyers for its product that are not currently being served. When soft-drink producers rationalized their independent bottler networks to make them more efficient and effective, both the soft-drink companies and the bottlers benefited. Overall value can also expand when firms work collaboratively with suppliers to improve coordination and limit unnecessary costs incurred in the supply chain. This lowers the inherent cost structure of the industry, allowing higher profit, greater demand through lower prices, or both. Or, agreeing on quality standards can bring up industry wide quality and service levels, and hence prices, benefiting rivals, suppliers, and customers.

Expanding the overall profit pool creates win-win opportunities for multiple industry participants. It can also reduce the risk of destructive rivalry that arises when incumbents attempt to shift bargaining power or capture more market share. However, expanding the pie does not reduce the importance of industry structure. How the expanded pie is divided will ultimately be determined by the five forces. The most successful companies are those that expand the industry profit pool in ways that allow them to share disproportionately in the benefits.

Defining the industry.

The five competitive forces also hold the key to defining the relevant industry (or industries) in which a company competes. Drawing industry boundaries correctly, around the arena in which competition actually takes place, will clarify the causes of profitability and the appropriate unit for setting strategy. A company needs a separate strategy for each distinct industry. Mistakes in industry definition made by competitors present opportunities for staking out superior strategic positions. (See the sidebar “Defining the Relevant Industry.”)

Competition and Value

The competitive forces reveal the drivers of industry competition. A company strategist who understands that competition extends well beyond existing rivals will detect wider competitive threats and be better equipped to address them. At the same time, thinking comprehensively about an industry’s structure can uncover opportunities: differences in customers, suppliers, substitutes, potential entrants, and rivals that can become the basis for distinct strategies yielding superior performance. In a world of more open competition and relentless change, it is more important than ever to think structurally about competition.

Typical Steps in Industry Analysis

Understanding industry structure is equally important for investors as for managers. The five competitive forces reveal whether an industry is truly attractive, and they help investors anticipate positive or negative shifts in industry structure before they are obvious. The five forces distinguish short-term blips from structural changes and allow investors to take advantage of undue pessimism or optimism. Those companies whose strategies have industry-transforming potential become far clearer. This deeper thinking about competition is a more powerful way to achieve genuine investment success than the financial projections and trend extrapolation that dominate today’s investment analysis.

Common Pitfalls

If both executives and investors looked at competition this way, capital markets would be a far more effective force for company success and economic prosperity. Executives and investors would both be focused on the same fundamentals that drive sustained profitability. The conversation between investors and executives would focus on the structural, not the transient. Imagine the improvement in company performance—and in the economy as a whole—if all the energy expended in “pleasing the Street” were redirected toward the factors that create true economic value.

1. For a discussion of the value chain framework, see Michael E. Porter, Competitive Advantage: Creating and Sustaining Superior Performance (The Free Press, 1998).

2. For a discussion of how internet technology improves the attractiveness of some industries while eroding the profitability of others, see Michael E. Porter, “Strategy and the Internet” (HBR, March 2001).

3. See, for instance, Adam M. Brandenburger and Barry J. Nalebuff, Co-opetition (Currency Doubleday, 1996).

canada pharmacy https://canadianpharmaceuticalsonline.home.blog/

You actually stated that perfectly.

Viagra levitra https://reallygoodemails.com/onlineviagra

You explained that very well!

Viagra 20 mg best price https://viagraonline.estranky.sk/clanky/viagra-without-prescription.html

Thanks a lot, Plenty of advice!

tadalafil 10 mg https://viagraonlineee.wordpress.com/

Kudos. Wonderful information.

tadalafil 20mg https://viagraonline.home.blog/

Many thanks. Numerous knowledge.

tadalafil 20mg https://viagraonlinee.livejournal.com/492.html

Perfectly expressed indeed. !

Viagra 5 mg funziona https://onlineviagra.flazio.com/

Regards, Ample info.

How does viagra work https://onlineviagra.fo.team/

Kudos! Loads of forum posts.

tadalafil https://www.kadenze.com/users/canadian-pharmaceuticals-for-usa-sales

Well spoken really. !

tadalafil 20mg https://linktr.ee/canadianpharmaceuticalsonline

With thanks! Numerous posts.

generic cialis https://disqus.com/home/forum/canadian-pharmaceuticals-online/

Appreciate it! Ample stuff.

cialis 20mg prix en pharmacie https://500px.com/p/canadianpharmaceuticalsonline

Superb write ups. Kudos.

cialis generic https://dailygram.com/index.php/blog/1155353/we-know-quite-a-bit-about-covid-19/

Wow loads of valuable material.

canada rx https://challonge.com/en/canadianpharmaceuticalsonlinemt

Amazing quite a lot of wonderful advice.

cialis tablets australia https://500px.com/p/listofcanadianpharmaceuticalsonline

Wow a good deal of fantastic knowledge.

tadalafil tablets https://www.seje.gov.mz/question/canadian-pharmacies-shipping-to-usa/

Appreciate it, Numerous material!

canadian pharmacys https://challonge.com/en/canadianpharmaciesshippingtousa

Terrific tips. Many thanks.

cialis tablets https://challonge.com/en/canadianpharmaceuticalsonlinetousa

Excellent forum posts. Many thanks.

canadian medications https://pinshape.com/users/2441403-canadian-pharmaceuticals-online

Nicely put. With thanks!

buy cialis https://www.scoop.it/topic/canadian-pharmaceuticals-online

You stated that exceptionally well.

cialis canada https://reallygoodemails.com/canadianpharmaceuticalsonline

Regards, Plenty of data.

buy cialis pinshape.com/users/2441621-canadian-pharmaceutical-companies

Appreciate it! An abundance of write ups.

cialis tablets australia https://pinshape.com/users/2441621-canadian-pharmaceutical-companies

Truly a good deal of good tips.

cialis uk https://reallygoodemails.com/canadianpharmaceuticalcompanies

Whoa quite a lot of excellent data.

stromectol from costco https://pinshape.com/users/2445987-order-stromectol-over-the-counter

You definitely made your point!

Viagra 20 mg best price https://reallygoodemails.com/orderstromectoloverthecounter

Nicely put, Appreciate it!

Viagra uk https://challonge.com/en/orderstromectoloverthecounter

Truly a lot of superb data!

Viagra dosage https://500px.com/p/orderstromectoloverthecounter

Nicely voiced indeed! !

Low cost viagra 20mg https://www.seje.gov.mz/question/order-stromectol-over-the-counter-6/

You said it adequately.!

order stromectol over the counter https://canadajobscenter.com/author/buystromectol/

Good facts. Kudos.

canada online pharmacies https://canadajobscenter.com/author/canadianpharmaceuticalsonline/

Thanks a lot, Very good stuff!

canada medication https://aoc.stamford.edu/profile/canadianpharmaceuticalsonline/

Superb posts. Many thanks.

canadian drug https://canadianpharmaceuticalsonline.bandcamp.com/releases

Kudos, Numerous tips.

Viagra or viagra https://ktqt.ftu.edu.vn/en/question list/canadian-pharmaceuticals-for-usa-sales/

Appreciate it! Ample write ups.

canadian pharmacy meds https://www.provenexpert.com/canadian-pharmaceuticals-online/

You mentioned that superbly!

Buy viagra online https://aoc.stamford.edu/profile/Stromectol/

Helpful material. Many thanks.

stromectol brasilien https://ktqt.ftu.edu.vn/en/question list/order-stromectol-over-the-counter-10/

Nicely put, Thank you!

stromectol over the counter https://orderstromectoloverthecounter.bandcamp.com/releases

With thanks. I appreciate this.

Viagra for daily use https://www.provenexpert.com/order-stromectol-over-the-counter12/

Very good knowledge. Cheers!

stromectol order https://www.repairanswers.net/question/order-stromectol-over-the-counter-2/

Thank you! Lots of data!

Viagra 20mg https://www.repairanswers.net/question/stromectol-order-online/

Very good material. Kudos!

buy stromectol uk https://canadajobscenter.com/author/arpreparof1989/

You actually expressed this perfectly!

buy stromectol scabies online https://aoc.stamford.edu/profile/goatunmantmen/

Amazing many of terrific data!

stromectol pill https://web904.com/stromectol-buy/

You expressed that exceptionally well.

Tadalafil https://web904.com/buy-ivermectin-online-fitndance/

Cheers! Good information.

Tadalafil 20 mg https://glycvimepedd.bandcamp.com/releases

Regards. An abundance of material!

Canadian viagra https://canadajobscenter.com/author/ereswasint/

Information well utilized..

Interactions for viagra https://aoc.stamford.edu/profile/hispennbackwin/

Seriously lots of wonderful info.

Viagra from canada https://bursuppsligme.bandcamp.com/releases

Excellent stuff. Appreciate it.

Viagra for sale https://pinshape.com/users/2461310-canadian-pharmacies-shipping-to-usa

Amazing lots of terrific facts.

Generic for viagra https://pinshape.com/users/2462760-order-stromectol-over-the-counter

You actually said it adequately!

Viagra canada https://pinshape.com/users/2462910-order-stromectol-online

Thanks! Loads of knowledge.

canada drug 500px.com/p/phraspilliti

Fine info. Cheers.

Buy viagra https://web904.com/canadian-pharmaceuticals-for-usa-sales/

Beneficial stuff. Many thanks.

Viagra online https://500px.com/p/skulogovid/?view=groups

Fantastic posts. Many thanks!

online pharmacies canada https://500px.com/p/bersavahi/?view=groups

Amazing loads of fantastic advice.

Viagra tablets australia https://reallygoodemails.com/canadianpharmaceuticalsonlineusa

Truly a good deal of useful information.

Viagra great britain https://www.provenexpert.com/canadian-pharmaceuticals-online-usa/

You expressed this really well.

Tadalafil 20 mg https://sanangelolive.com/members/pharmaceuticals

Superb posts, Thank you.

5 mg viagra coupon printable https://melaninterest.com/user/canadian-pharmaceuticals-online/?view=likes

Helpful information. Thanks!

Buy viagra online https://haikudeck.com/canadian-pharmaceuticals-online-personal-presentation-827506e003

Thanks a lot! Terrific information.

Viagra rezeptfrei https://buyersguide.americanbar.org/profile/420642/0

Thanks a lot! I enjoy this!

Viagra 5 mg https://experiment.com/users/canadianpharmacy

You suggested that exceptionally well.

Viagra 5mg prix https://slides.com/canadianpharmaceuticalsonline

Cheers. I enjoy it.

Viagra bula https://challonge.com/esapenti

You mentioned it exceptionally well.

Viagra kaufen https://challonge.com/gotsembpertvil

Amazing quite a lot of excellent advice.

Buy viagra https://challonge.com/citlitigolf

Terrific information, Thanks.

Generic for viagra https://order-stromectol-over-the-counter.estranky.cz/clanky/order-stromectol-over-the-counter.html

Thanks. Awesome information!

reaction au stromectol https://soncheebarxu.estranky.cz/clanky/stromectol-for-head-lice.html

Amazing information. Thanks a lot.

Viagra 5mg https://lehyriwor.estranky.sk/clanky/stromectol-cream.html

You actually revealed this fantastically.

Cheap viagra https://dsdgbvda.zombeek.cz/

Very good postings. Regards!

stromectol france https://inflavnena.zombeek.cz/

Amazing content. Thanks!

canadian rx https://www.myscrsdirectory.com/profile/421708/0

Excellent data. Thanks!

Viagra from canada https://supplier.ihrsa.org/profile/421717/0

Whoa loads of great knowledge!

Viagra 20mg https://wefbuyersguide.wef.org/profile/421914/0

Kudos! Lots of postings.

Tadalafil https://legalmarketplace.alanet.org/profile/421920/0

Thanks! Quite a lot of data!

drugstore online https://moaamein.nacda.com/profile/422018/0

Thanks! An abundance of material!

online drug store https://www.audiologysolutionsnetwork.org/profile/422019/0

Fantastic facts. Regards!

Online viagra https://network.myscrs.org/profile/422020/0

Awesome information. Thank you.

Viagra 5 mg https://sanangelolive.com/members/canadianpharmaceuticalsonlineusa

Perfectly voiced certainly. .

stromectol pharmacokinetics https://sanangelolive.com/members/girsagerea

You made your point very nicely.!

Viagra reviews https://www.ecosia.org/search?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

With thanks. I enjoy it!

Viagra vs viagra https://www.mojomarketplace.com/user/Canadianpharmaceuticalsonline-EkugcJDMYH

Many thanks. I appreciate it.

Canadian Pharmacy USA https://seedandspark.com/user/canadian-pharmaceuticals-online

Many thanks, I value it!

best canadian pharmacy https://www.giantbomb.com/profile/canadapharmacy/blog/canadian-pharmaceuticals-online/265652/

Thanks, Awesome information!

Interactions for viagra https://feeds.feedburner.com/bing/Canadian-pharmaceuticals-online

Many thanks, I enjoy this.

Viagra 5mg https://search.gmx.com/web/result?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

Regards! I value it!

canadian medications https://search.seznam.cz/?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

You mentioned this exceptionally well.

Tadalafil 20 mg https://sanangelolive.com/members/unsafiri

Great info. Thank you.

Viagra generico online

Thank you, I appreciate it.

Viagra alternative https://swisscows.com/en/web?query=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

Nicely put. Thanks!

canadian pharmacys https://www.dogpile.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

You reported it wonderfully.

Canadian viagra

Kudos! Ample write ups.

Viagra daily https://search.givewater.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

You made your position very effectively.!

canada medication https://www.bakespace.com/members/profile/?anadian pharmaceuticals for usa sales/1541108/

Incredible plenty of awesome tips.

canada drugs online

Very good write ups, Thanks.

canadian drug https://results.excite.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

You actually suggested this superbly.

canadian pharmacies online https://www.infospace.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

Nicely put. With thanks!

Viagra 5 mg https://headwayapp.co/canadianppharmacy-changelog

You expressed it fantastically.

canada medication https://results.excite.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

With thanks! I enjoy it.

Buy viagra online https://canadianpharmaceuticalsonline.as.me/schedule.php

Awesome data. Cheers!

Tadalafil 20 mg https://feeds.feedburner.com/bing/stromectolnoprescription

Great facts, Appreciate it!

Viagra cost https://reallygoodemails.com/orderstromectoloverthecounterusa

You suggested that wonderfully!

Viagra cost https://aoc.stamford.edu/profile/cliclecnotes/

With thanks, An abundance of postings.

Viagra kaufen https://pinshape.com/users/2491694-buy-stromectol-fitndance

Excellent write ups. With thanks.

Viagra generic https://www.provenexpert.com/medicament-stromectol/

You actually mentioned it terrifically!

Viagra vs viagra https://challonge.com/bunmiconglours

Perfectly voiced without a doubt. .

Viagra 20 mg best price https://theosipostmouths.estranky.cz/clanky/stromectol-biam.html

Perfectly spoken indeed. !

Viagra levitra https://tropkefacon.estranky.sk/clanky/buy-ivermectin-fitndance.html

Thanks a lot. Lots of advice!

canadian mail order pharmacies https://www.midi.org/forum/profile/89266-canadianpharmaceuticalsonline

Great advice. Kudos!

Viagra pills https://dramamhinca.zombeek.cz/

Thanks a lot. I appreciate it!

Viagra or viagra https://sanangelolive.com/members/thisphophehand

Cheers. I appreciate it.

Discount viagra https://motocom.co/demos/netw5/askme/question/canadian-pharmaceuticals-online-5/

You have made the point.

canadian pharmacy meds https://www.infospace.com/serp?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

Regards. Lots of info.

Viagra pills https://zencastr.com/@pharmaceuticals

Awesome advice. Thank you.

stromectol composition https://aleserme.estranky.sk/clanky/stromectol-espana.html

Cheers. I like it.

Online viagra https://orderstromectoloverthecounter.mystrikingly.com/

Nicely voiced really. !

stromectol australia https://stromectoloverthecounter.wordpress.com/

Nicely expressed of course. .

stromectol medication https://buystromectol.livejournal.com/421.html

Thank you! Quite a lot of content!

Viagra pills https://orderstromectoloverthecounter.flazio.com/

Thanks a lot. I like it!

canadian pharmacies https://search.lycos.com/web/?q=“My Canadian Pharmacy – Extensive Assortment of Medications – 2022”

Many thanks, I like this!

canadian pharmacy king https://conifer.rhizome.org/pharmaceuticals

Great content. Thank you.

Buy viagra https://telegra.ph/Order-Stromectol-over-the-counter-10-29

You definitely made the point!

purchase stromectol https://graph.org/Order-Stromectol-over-the-counter-10-29-2

Appreciate it. Lots of postings!

Viagra vs viagra https://orderstromectoloverthecounter.fo.team/

You actually expressed that very well!

Viagra vs viagra https://orderstromectoloverthecounter.proweb.cz/

You said it perfectly..

Viagra online https://orderstromectoloverthecounter.nethouse.ru/

With thanks! Excellent stuff!

Viagra generico https://sandbox.zenodo.org/communities/canadianpharmaceuticalsonline/

You suggested it very well.

Viagra reviews https://demo.socialengine.com/blogs/2403/1227/canadian-pharmaceuticals-online

Thank you, Plenty of information.

Buy viagra https://pharmaceuticals.cgsociety.org/jvcc/canadian-pharmaceuti

Useful forum posts. Many thanks!

Viagra generique https://taylorhicks.ning.com/photo/albums/best-canadian-pharmaceuticals-online

This is nicely put! !

5 mg viagra coupon printable https://my.afcpe.org/forums/discussion/discussions/reputable-canadian-pharmaceuticals-online

You made your position extremely effectively!.

Viagra 5mg https://www.dibiz.com/ndeapq

Seriously a lot of excellent tips.

Viagra bula https://www.podcasts.com/canadian-pharmacies-shipping-to-usa

Nicely put. Appreciate it.

Viagra 20 mg https://canadianpharmaceuticals.educatorpages.com/pages/canadian-pharmacies-shipping-to-usa

Excellent tips. Thank you.

Viagra uk https://soundcloud.com/canadian-pharmacy

Regards, Loads of forum posts!

Canadian viagra https://peatix.com/user/14373921/view

Fine advice. Thanks a lot!

Tadalafil https://www.cakeresume.com/me/best-canadian-pharmaceuticals-online

Really a good deal of wonderful advice.

Viagra online https://dragonballwiki.net/forum/canadian-pharmaceuticals-online-safe/

Thank you! Quite a lot of stuff!

Viagra dosage https://the-dots.com/projects/covid-19-in-seven-little-words-848643

Amazing posts. Many thanks!

canadian pharmacys https://jemi.so/canadian-pharmacies-shipping-to-usa

You actually stated it really well!

Viagra tablets australia https://www.homify.com/ideabooks/9099923/reputable-canadian-pharmaceuticals-online

You made the point.

Viagra great britain https://medium.com/@pharmaceuticalsonline/canadian-pharmaceutical-drugstore-2503e21730a5

You actually mentioned that really well!

cialis canadian pharmacy https://infogram.com/canadian-pharmacies-shipping-to-usa-1h1749v1jry1q6z

Many thanks! A good amount of knowledge!

best canadian mail order pharmacies https://pinshape.com/users/2507399-best-canadian-pharmaceuticals-online

You actually suggested that fantastically.

Viagra 20mg https://aoc.stamford.edu/profile/upogunem/

Seriously plenty of wonderful material.

Viagra 5mg prix https://500px.com/p/maybenseiprep/?view=groups

You’ve made your position quite clearly.!

Viagra 5 mg https://challonge.com/ebtortety

You have made your point extremely effectively..

Viagra for daily use https://sacajegi.estranky.cz/clanky/online-medicine-shopping.html

Good information. Regards!

Viagra daily https://speedopoflet.estranky.sk/clanky/international-pharmacy.html

You expressed that exceptionally well!

Viagra generique https://dustpontisrhos.zombeek.cz/

Thanks a lot! Loads of forum posts!

Viagra coupon https://sanangelolive.com/members/maiworkgendty

You actually reported it very well.

best canadian pharmacies online https://issuu.com/lustgavalar

Cheers, Loads of posts.

Tadalafil 5mg https://calendly.com/canadianpharmaceuticalsonline/onlinepharmacy

Very good advice. Appreciate it.

Viagra reviews https://aoc.stamford.edu/profile/uxertodo/

You said it very well..

Viagra tablets https://www.wattpad.com/user/Canadianpharmacy

You explained that really well!

Viagra generico https://pinshape.com/users/2510246-medicine-online-shopping

You actually mentioned this perfectly.

Viagra generic https://500px.com/p/reisupvertketk/?view=groups

Thanks. Plenty of posts.

online canadian pharmacies https://www.provenexpert.com/online-order-medicine/

Many thanks, Good stuff.

Viagra levitra https://challonge.com/ebocivid

Reliable write ups. Cheers!

Viagra great britain https://obsusilli.zombeek.cz/

Seriously a good deal of superb information!

Buy viagra online https://sanangelolive.com/members/contikegel

Truly a good deal of wonderful material.

canadian viagra https://rentry.co/canadianpharmaceuticalsonline

Beneficial advice. Thanks a lot.

pharmacy canada https://tawk.to/canadianpharmaceuticalsonline

This is nicely put. !

Viagra purchasing https://canadianpharmaceuticalsonline.tawk.help/article/canadian-pharmacies-shipping-to-usa

You revealed it well!

canadian prescription drugstore https://sway.office.com/bwqoJDkPTZku0kFA

Regards. I value it.

best canadian pharmacy https://canadianpharmaceuticalsonline.eventsmart.com/2022/11/20/canadian-pharmaceuticals-for-usa-sales/

Point well utilized.!

Cheap viagra https://suppdentcanchurch.estranky.cz/clanky/online-medicine-order-discount.html

You actually said this perfectly.

Viagra vs viagra vs levitra https://aoc.stamford.edu/profile/tosenbenlren/

With thanks. Quite a lot of postings!

canadadrugs https://pinshape.com/users/2513487-online-medicine-shopping

You have made your point!

Viagra 5mg prix https://500px.com/p/meyvancohurt/?view=groups

With thanks. Plenty of information.

canada drugs online https://www.provenexpert.com/pharmacy-online/

Seriously loads of very good material!

canada pharmacy online https://challonge.com/townsiglutep

You actually mentioned that adequately!

Tadalafil 20 mg https://appieloku.estranky.cz/clanky/online-medicine-to-buy.html

Seriously many of excellent knowledge.

Interactions for viagra https://scisevitrid.estranky.sk/clanky/canada-pharmacies.html

Fantastic information. Many thanks.

Viagra levitra https://brujagflysban.zombeek.cz/

Many thanks, Useful stuff.

Canadian viagra https://500px.com/p/stofovinin/?view=groups

Terrific advice. Many thanks!

Buy generic viagra https://www.provenexpert.com/best-erectile-pills/

You made the point!

Viagra generic https://challonge.com/afersparun

Incredible quite a lot of amazing facts!

Viagra generika https://plancaticam.estranky.cz/clanky/best-drugs-for-ed.html

You mentioned that adequately.

Viagra manufacturer coupon https://piesapalbe.estranky.sk/clanky/buy-erectile-dysfunction-medications-online.html

Tips effectively taken!!

erectile dysfunction medications https://wallsawadar.zombeek.cz/

You actually said this adequately!

canadian drugstore https://www.cakeresume.com/me/canadian-pharmaceuticals-online/

Thank you, I like this.

Viagra 20 mg best price https://canadianpharmaceuticalsonline.studio.site/

Useful posts. Thanks.